Material Weaknesses — A Potential Obstacle to IPO Success

.png)

During the IPO journey, accounting and finance teams play an outsized role in determining a company’s readiness as well as its potential for IPO success.

Amidst all the headwinds that companies will already face while going public, material weaknesses are of the most haunting — a direct indication of procedural failure on the behalf of the accounting team. Even worse, as the IPO market begins to warm up, more teams are disclosing material weaknesses than ever before.

With insights from Big 4 audit firms, we breakdown the impact that material weaknesses have on IPO candidates and how these teams should look to remediate their pain points.

What is a material weakness?

The SEC defines a material weakness as the following:

“A material weakness is a deficiency, or combination of deficiencies, in ICFR such that there is a reasonable possibility that a material misstatement of the company's annual or interim financial statements will not be prevented or detected on a timely basis.”

Simply stated, a material weakness refers to a flaw or gap in a company's internal controls that could allow for material errors in financial reporting. Ironically, material weaknesses are not about there being any current errors at all; they symbolize a lack of integrity in an accounting team’s controls or risk prevention techniques. Just like a school fire drill, teams need to have strong processes even in the absence of a fire.

Here are notable examples illustrating this concept:

1. Insurance Company Case (2019): MetLife faced a material weakness due to internal control failures in their annuities business. They had a long-standing policy that allowed them to assume customers who did not respond to two mailings over five years were deceased or untraceable. This flawed assumption led to the company inaccurately freeing up funds set aside for claims, ultimately resulting in a $10 million settlement with the SEC.

2. Costco Incident (2018): Costco identified unauthorized access to its financial reporting systems. Although no actual misstatements were found, the potential for errors led the company to classify this as a material weakness.This decision negatively impacted their stock price, demonstrating how even the possibility of control failures can have significant market consequences.

Given the serious consequences tied into material weaknesses, ensuring that these weaknesses are prevented or swiftly addressed is not just a matter of good practice—it's essential for the financial health and credibility of the company.

Current state of material weaknesses & IPOs

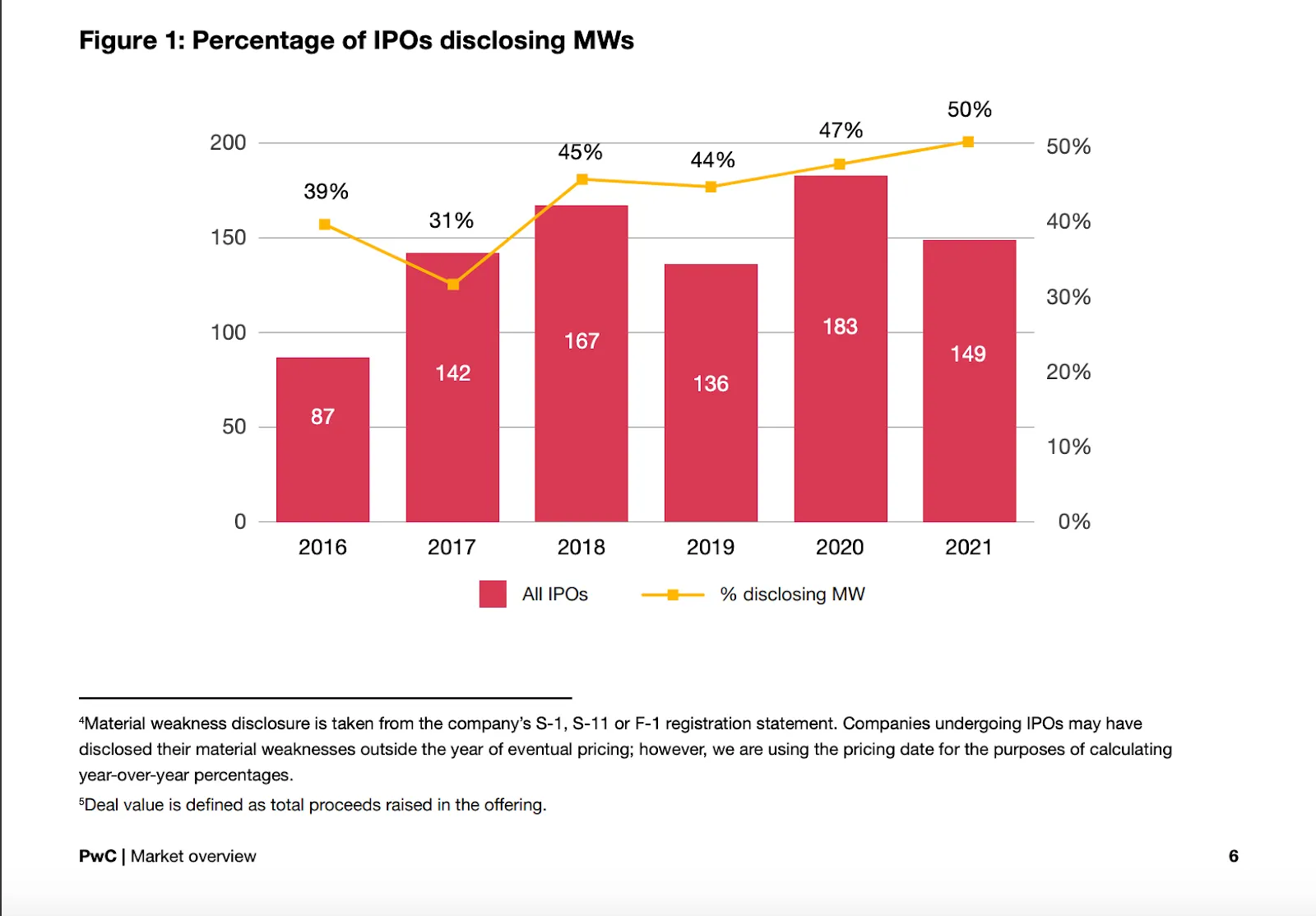

If your company’s thinking about a potential IPO, here’s some tough news: based on recent trends, you’re more likely to go public with a material weakness than not. In PwC’s report on material weakness disclosures, they stated that the rate of material weakness disclosure in IPOs has increased significantly since 2017 (see below) and KPMG found that 58% of IPOs in 2022 had a material weakness in their initial S-1/S-4/F-1 documentation.

These additional statistics from PwC add color to the ongoing boom in material weaknesses:

- Despite a traditional correlation between smaller company deal size and revenue with a higher likelihood for material weaknesses, the trend now spans companies of all sizes.

- In the technology, media, and telecommunications sector, an average of 55% of the companies that went public disclosed at least one material weakness, higher than the average of 43% across all sectors.

- PwC sees a possible cause being the fact that “these companies tend to be relatively smaller in size, less mature and in an early stage of development.”

- In 2021, 74% of foreign private issuers (F-1) disclosed material weaknesses in their IPOs compared to only 40% of domestic issuers (S-1).

Reasons for Material Weakness

Naturally, one must wonder what’s driving the uptick in material weaknesses as well as the root accounting issues at play.

Accounting Issues

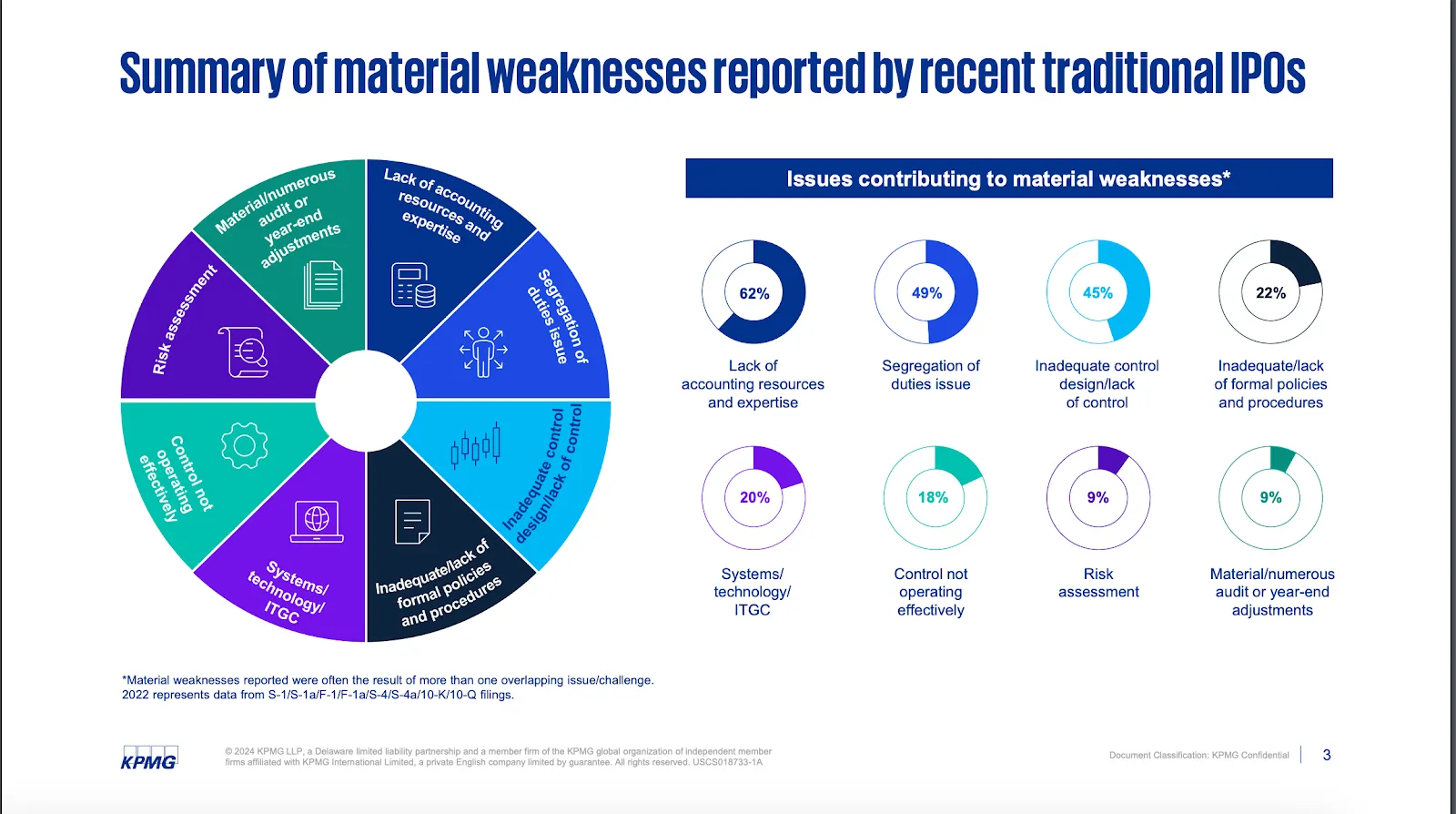

This chart from KPMG’s 2023 study depicts the issues contributing most to material weakness. The top three by a solid margin are the following: lack of accounting resources & expertise, segregation of duties, and inadequate control design/lack of control.

As for where these issues pop up, they span a series of common accounting processes — tax, revenue, equity, complex transactions, and more.

The biggest culprit, however, is that of financial close & reporting: even accounting for the fact that material weaknesses could span multiple processes, 70% of material weaknesses pertain to the financial reporting related to periodic and annual closes. The next closest — systems (IT systems, etc.) — only touches 26% of material weaknesses.

Underlying Reasons

In the report’s “Key Takeaways”, KPMG makes these statements regarding material weaknesses:

“ Material weaknesses primarily fall in areas of accounting complexity that require the use of estimates and judgment, such as financial reporting, systems, control environment…”

“Private companies often do not have the in-house expertise and/or resources are stretched too thin to appropriately identify, analyze, and account for complex transactions.”

Given these analyses, it’s clear that the ongoing accounting shortage is having an outsized impact on businesses’ ability to deliver accurate data and establish strong internal processes. Not only are companies unable to find the personnel to support their IPO mission, they are lacking accountants with the appropriate skills to make the correct calls on highly subjective accounting matters.

Why Preventing Material Weakness is Crucial for Businesses

Material weaknesses in internal controls can have severe consequences for businesses.

Potential Damage to Credit Ratings and Share Prices

When material weaknesses remain unchecked, they can negatively affect a company's credit ratings and share prices. Companies may face increased borrowing costs as lenders view them as riskier investments, and investors may sell their shares if they perceive the company as financially unstable.

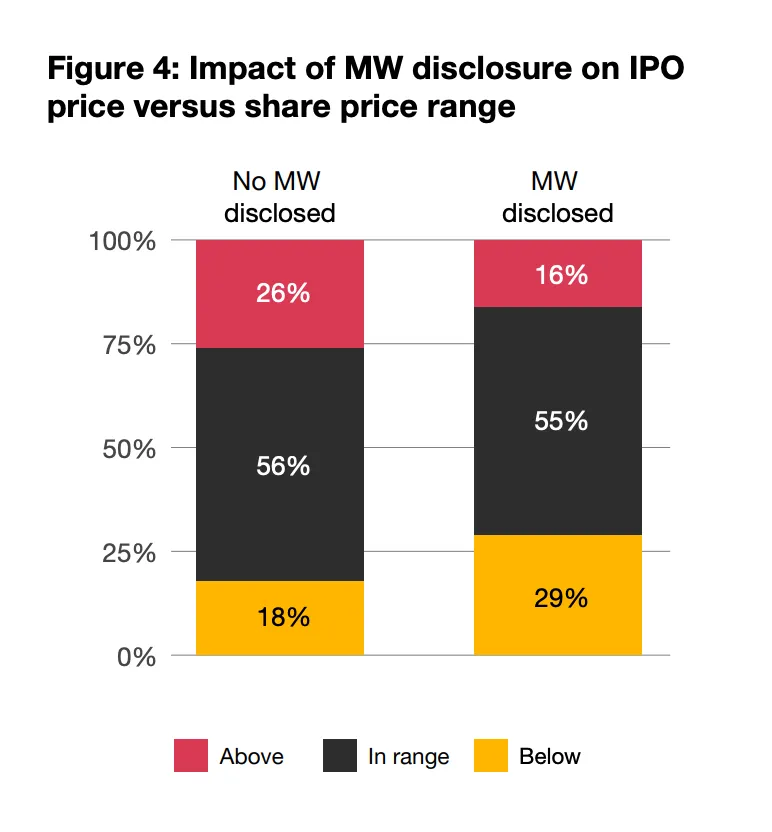

This chart from PwC illustrates how material weakness disclosures make teams less likely to IPO above their share price range and more likely to actually go below:

Increased Audit Fees and Loss of Investor Confidence

Material weaknesses often lead to increased audit fees. Auditors may need to perform additional procedures to assess and address these weaknesses, resulting in higher costs for the company. Moreover, persistent weaknesses can erode investor confidence, making them hesitant to continue their support.

Loss in Credibility of Management

Management may come under intense scrutiny from auditors, regulators, and stakeholders when material weaknesses are reported. This scrutiny can lead to disciplinary actions against management and increased oversight costs. The perception that management failed to maintain adequate controls can further diminish their credibility.

Long-Term Financial Health and Valuation Risks

The presence of material weaknesses poses risks to a company's long-term financial health and valuation. Consistent errors in financial reporting can lead to:

- Undervalued or overvalued assets: Misstatements may cause investors to misjudge the true value of the company.

- Financial instability: Persistent weaknesses can hinder strategic decision-making and growth opportunities.

In conclusion, preventing material weaknesses is vital for safeguarding a company's financial integrity, maintaining investor confidence, and ensuring compliance with legal requirements. By taking proactive measures, businesses can avoid the costly repercussions associated with material weaknesses.

Put Your Team on the Road to IPO

Remediation & Prevention of Material Weaknesses

Perhaps the silver lining of the increasing trend of material weaknesses is the fact that other companies now have a blueprint for how to either remediate existing material weaknesses or institute prevention and risk assessment plans to avoid them.

When businesses disclose material weaknesses, they almost always include a remediation plan that lists the strategies the business will take to address the issue.

In this example, the company mentions these strategies amongst others: hiring a Chief Accounting Officer, performing an IT process risk and controls assessment, and evaluating segregation of duties within key processes and controls.

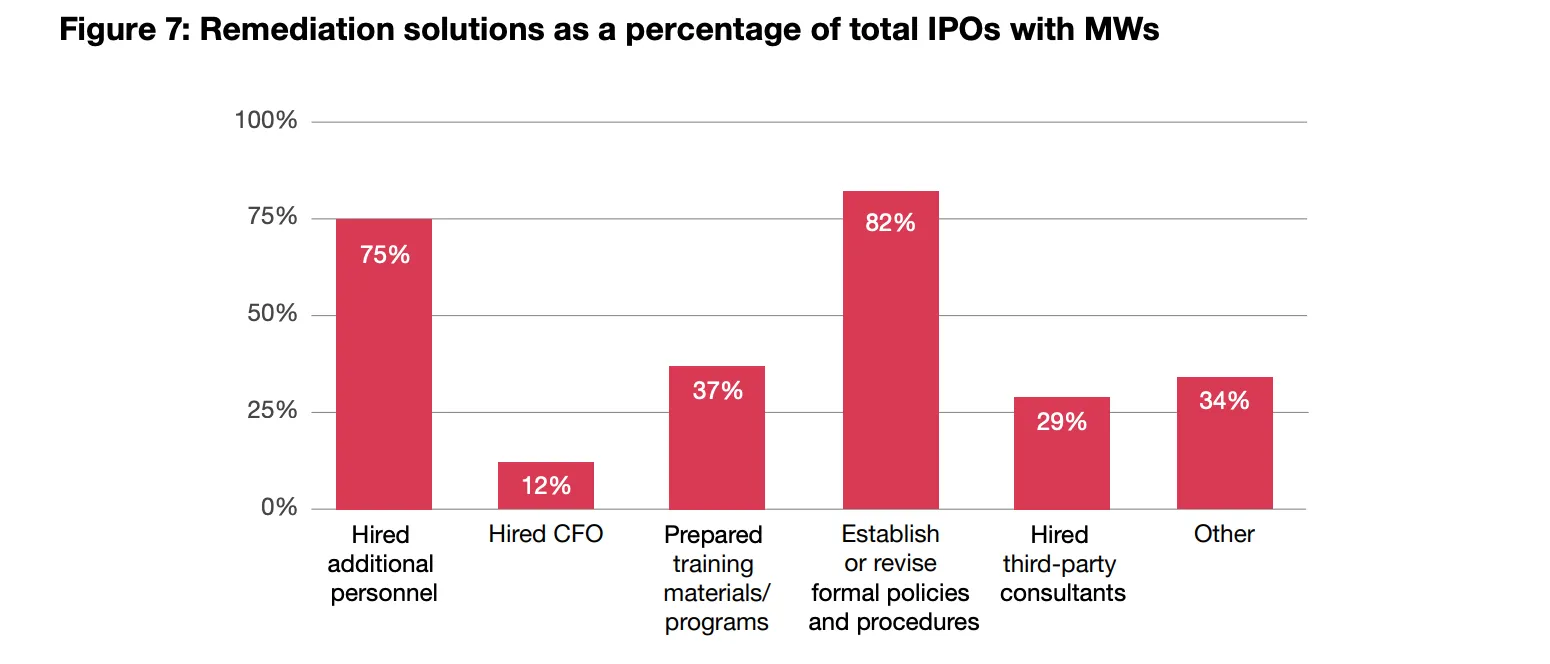

PwC reports that the most common solutions are revising formal policies and procedures and hiring additional personnel.

Given these stats, here’s how teams should think of addressing material weaknesses or developing processes to prevent them:

Assess Your Control Environment

A robust control environment is the backbone of preventing material weaknesses. Continuous validation and remediation of internal controls ensure that they function effectively. Regular checks on controls can catch issues before they escalate, and a culture of accountability encourages employees to adhere to controls.

Outline Strong Policies and Processes

Establishing clear policies and procedures helps mitigate risks, and revising existing policies can clear up ongoing accounting bottlenecks or confusion. These guidelines serve as a roadmap for employees, detailing what steps to take in various financial scenarios. By investing in strong practices early, teams can also better anticipate how they may need to scale or change their procedures as they approach an IPO.

Asses and Implement Appropriate Technology

Teams should consistently assess their accounting tech stack to ensure that they have the tools to address procedural gaps. For teams struggling to maintain a single source of truth, using close software to centralize documentation makes it easier to track and manage financial data over time.

Numeric is a best-in-class close solution that helps to drive completeness and accuracy of financial data in addition to managing the close process. Numeric brings in transaction-level details from your ERP to enhance the software’s automated reconciliations, variance analysis, and proactive transaction monitoring—features designed to ensure each close is thorough and audit-ready. Beyond the data, teams can maintain complete close visibility with their own customized month-end close checklist and a complete activity trail that delights auditors and management alike.

Invest in Personnel

Teams of all sizes are feeling the strain of the accounting shortage. As such, it could make the most sense to create training programs for current employees to increase accounting expertise and judgment around processes, complex accounting issues, and more.

Companies should also consider how to implement AI to give their accounting teams leverage and the time to focus on more nuanced accounting tasks. In manycircumstances, bringing on a CAO or exec with public accounting experience may be most beneficial for ironing out internal company issues.

Hire Third-Party Experts

If you’re struggling to envision how you can improve your accounting processes while still having the time to actually do these same processes, then it could be worth hiring outside help.

Bringing in third-party consultants offers fresh insights and expertise in process and controls. While costly, these experts can provide an unbiased assessment of your systems, highlighting areas for improvement and helping to prevent potential weaknesses.

By implementing these strategies, organizations can create a framework to prevent and detect material weaknesses, ensuring financial reporting remains accurate and dependable in the pursuit of IPO readiness.

The Bottom Line

Addressing material weaknesses is a crucial step for companies preparing for an IPO, as these deficiencies pose significant risks to financial stability and market perception.

By strengthening internal controls, investing in skilled personnel, and leveraging technology, businesses can build a more resilient foundation for financial reporting. With a proactive approach to risk management, companies can not only enhance their IPO readiness but also foster long-term investor confidence and financial integrity.

Related Content

.png)

.png)

Finance Process Improvement: A Comprehensive Guide For Mid-Market And Enterprise Teams

Finance process improvement is how you close the gap between what the business expects from finance and what your current workflows can actually deliver. This guide covers which processes to improve first, how to assess your current state, how to build a phased roadmap, and where technology fits in.

.png)

Finance Team Structure: How To Build A Modern Finance Organization

How to design a finance team structure that scales alongside your business — covering roles, reporting lines, structural models, centralization tradeoffs, and design principles for SaaS and high-growth companies.