Minding the Gaps: How to Calculate Materiality Thresholds in Accounting

Bad accounting begins with bad numbers. Not only does inaccurate financial data confuse teams internally, but it leads to incomplete reporting as well. And what does incomplete reporting lead to? Simply put, more problems than your business could or should ever want to have.

While teams should strive for financial information that’s as precise as possible, the accounting powers that be – the SEC, IASB, and FASB to name a few – allow for some leniency. This idea, known as a materiality threshold, determines just how much businesses should pay attention to their discrepancies.

This blog will guide you through the concept of materiality thresholds, their importance, and how they differ under both GAAP and IFRS. Understanding these thresholds is crucial for numerous financial operations – especially balance sheet reconciliations, P&L management, and general ledger reconciliations – but even more so for anyone involved in a company’s financial reporting and auditing.

What is a Materiality Threshold?

A materiality threshold in accounting marks the point at which information influences economic decision-making. This means that if an omission or error in financial statements could change decisions made by investors, creditors, or other users, it’s considered material.

Accounting teams and their auditors use this threshold as an internal control to decide which errors or omissions are substantial enough to require correction. By focusing on material discrepancies, businesses help to present a clearer and more accurate picture of their financial position.

Simply put, materiality thresholds help determine whether or not a difference really matters.

Imagine you're looking at two discrepancies in reported transactions: one expenditure for $1000 and another for $1,000,000. The $1000 transaction probably won't change how you view a company's finances, but the $1,000,000 one definitely could.

When are Materiality Thresholds used?

Materiality thresholds guide financial reporting, auditing, and management decisions, and their use varies across different scenarios:

- Financial Statement Preparation: Accountants use them to assess whether to include or adjust certain transactions or errors.

- Flux Analyses: Materiality thresholds help teams to key in on where to perform flux analysis, specifically if an account’s changes surpass the threshold.

- Audits: Auditors use materiality to determine if misstatements are significant enough to impact the reliability of the financial statements.

- Internal Controls: Companies apply materiality thresholds when designing internal controls to focus on areas that could materially affect financial reporting.

What is Performance Materiality?

Auditors require one materiality amount for the financial statements, but a separate materiality for individual accounts. This latter materiality, known as the performance materiality, typically is 50-75% of the materiality for financial statements.

The performance materiality serves as a control to help ensure that the total of any undetected or uncorrected misstatements doesn’t exceed the overall materiality for financial statements.

Using Numeric for Setting Materiality Thresholds

With Numeric, teams see a material difference (we’re sorry, but you knew it was coming) in keeping up with materiality.

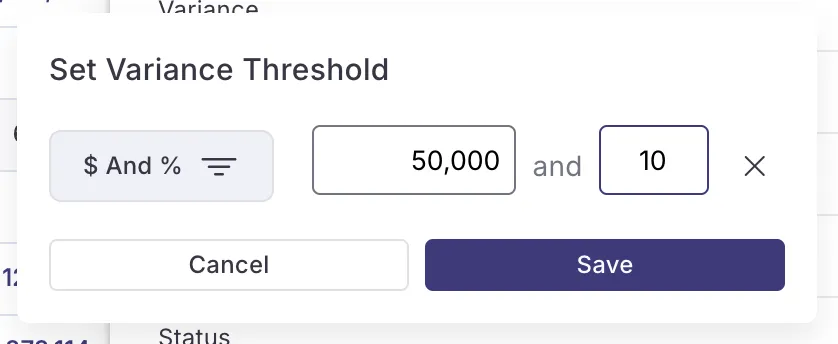

Numeric makes it easy to implement materiality thresholds on an account-by-account level for balance sheet reconciliations – teams can bring in whatever method they typically use to gauge materiality – a dollar amount, a percentage, or a combination of the two. Account balances that are above the threshold will display red, while immaterial variances are green and can be toggled on and off from your dashboard.

It’s 2024 — don’t waste your time manually scouring your financial statements for material differences.

Instead, rely on automation technology to efficiently identify discrepancies in your balance sheet or what’s driving MoM / QoQ / YoY changes on your income statement. Numeric pulls in GL data from your ERP, allowing you to dive into the transaction-level details behind each account. Click into any account that’s above the materiality levels, and you’ll see the culprit transaction highlighted for easy correction.

Audit-ready? Check. Highly visible? Check. Adaptable for your business? Check.

Looking for even more month-end "material"?

Check out our e-book, Mastering the Month-End Close, where accounting leaders from companies like Ramp, Mercury, and UserGems share their insights on just exactly how they run a best-in-class close.

Reduce audit headaches with a clear audit trail

.png)

How do materiality thresholds differ between GAAP and IFRS?

GAAP Approach to Materiality Threshold

Definition: Under GAAP (Generally Accepted Accounting Principles), materiality is defined as the magnitude of an omission or misstatement of accounting information that, in light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would have been changed or influenced by the inclusion or correction of the item.

Impact on Financial Reporting: Since GAAP focuses on the potential influence on the judgment of a reasonable person, this often results in a more rules-based approach where specific thresholds and guidelines are followed.

IFRS Approach to Materiality Threshold

Definition: For IFRS (International Financial Reporting Standards), information is considered material if omitting, misstating, or obscuring it could reasonably be expected to influence decisions made by the primary users of the financial statements, including investors, lenders, and other creditors.

Impact on Financial Reporting: IFRS adopts a more principles-based approach, emphasizing the importance of materiality in the context of the overall financial statements. This can lead to more judgment-based assessments, considering both the quantitative and qualitative aspects of the information.

Examples Illustrating IFRS vs. GAAP Materiality

Overall, we can think of GAAP as the standard that uses more rigid thresholds for materiality while IFRS considers context and qualitative factors. To understand these differences better, let’s look at some examples.

- Quantitative Materiality

- GAAP Example: A company may only consider a transaction material if it represents more than 5% of net income. This rule-based threshold ensures consistency.

- IFRS Example: Under IFRS, for the same transaction, even if less than 5% could influence the decision of a primary user, it might be deemed material.

- Qualitative Materiality

- GAAP Example: An error involving a misstatement of $10,000 in a large corporation might be considered immaterial based on quantitative thresholds alone.

- IFRS Example: If the $10,000 misstatement involved fraudulent activity, IFRS would likely consider it material due to the qualitative impact on the integrity of the financial statements.

Why Do Materiality Thresholds Matter?

The materiality threshold is central to financial reporting and auditing as it ensures that financial statements reflect a company's true financial status. These are some more detailed reasons why teams should care about their materiality thresholds.

Cultivating Data Accuracy

By setting materiality thresholds, teams can identify and correct errors that could mislead stakeholders. As such, materiality thresholds are another way to verify that financial reports are free from major inaccuracies as well as reduce audit risk.

Maintaining Efficiency in Reporting and Audit Procedures

Consider a financial statement filled with every tiny transaction a company makes –it would be overwhelming and unhelpful. Because an audit of financial statements with every single transaction is neither practical nor efficient, materiality thresholds help businesses to better think about what financial data to report and they streamline financial statements for auditors.

An audit of every single transaction a company makes would be overwhelming and incredibly time inefficient. In an effort to create efficiencies, materiality thresholds help businesses to better think about what financial data to report and they streamline financial statements for auditors.

Establishing Trust for Stakeholders

Different users rely on financial statements to make informed decisions. Some common users of financial statements include:

- Shareholders: Interested in profitability and overall financial performance.

- Management: Uses this data for strategic planning.

- Regulating Entities: Ensure compliance with financial regulations.

Understanding and applying the materiality threshold ensures that financial statements are both useful and reliable, guiding stakeholders toward sound economic decisions.

Legal Implications and Compliance with Auditing Standards

Companies must follow standards set by bodies like the SEC and FASB; otherwise, non-compliance can lead to legal penalties and loss of reputation. Meeting legal standards ensures that financial reports are transparent and reliable.

What is the Criteria for Determining Materiality Thresholds?

Since accounting standards don’t require any specific quantities for materiality, determining materiality thresholds becomes more art than science. There is no one-size-fits-all rule – determining overall materiality for your company depends on your company size, the types of transactions being studied, what your audit committee decides, and more.

As a starting point, teams can abide by some common rules of thumb when thinking about defining their materiality.

Quantitative and Qualitative Factors

Quantitative and qualitative factors both play pivotal roles in setting materiality thresholds.

Quantitative Principle – Absolute vs. Relative Amounts

- Absolute Amounts: These are fixed dollar amounts. For example, a $10,000 error might be material for a small business but insignificant for a multinational corporation.

- Relative Amounts: These are percentages of key financial metrics like revenue or assets. For instance, a 5% error in net income might be material regardless of the absolute amount.

To illustrate, consider the following examples:

- Small Business

- Absolute Amount: $10,000 might be the threshold.

- Relative Amount: 1% of revenue could be material.

- Large Corporation

- Absolute Amount: $1,000,000 might be the threshold.

- Relative Amount: 0.5% of total assets could be material.

Qualitative Principle – Considering Transaction Context

Even transactions that might seem immaterial by quantitative measures may become material when context is added. These are common qualitative considerations:

- Reputation: Errors impacting a company's reputation or compliance with laws can be material even if the amounts are small.

- Regulatory Impact: Certain transactions might be more significant due to regulatory requirements.

- Fraud: Even small errors can be material if they involve fraud, as they can indicate deeper issues.

By understanding and applying these principles, accountants can set appropriate materiality thresholds, ensuring that financial statements are both accurate and useful.

Quantitative Methods for Determining Materiality

Single Rule Methods

Single rule methods offer straightforward ways to set materiality thresholds. These methods use specific percentages applied to key financial metrics. Here are some common single rule methods:

- 5% of Pre-Tax Income: This method considers 5% of a company's pre-tax income as the materiality threshold. For a company with a pre-tax income of $2 million, the materiality threshold would be $100,000.

- 0.5% of Total Assets: This approach sets the threshold at 0.5% of the company's total assets. For a business with $100 million in assets, the materiality threshold would be $500,000.

- 1% of Shareholders’ Equity: Using 1% of shareholders' equity is another common method. If a company has $50 million in equity, the threshold would be $500,000.

- 1% of Total Revenue: This method applies 1% to the total revenue. For example, if a company earns $300 million in revenue, the materiality threshold would be $3 million.

Variable Size Rule Methods

Variable size rule methods offer more flexibility by adjusting percentages based on the company's size or profitability. These methods consider multiple factors to set a more accurate materiality threshold

Different Percentages Based on Gross Profit Ranges

This method adjusts the percentage based on the range of gross profit. For instance:

- 2% to 5% of Gross Profit (if less than $20,000): Smaller companies with gross profits below $20,000 might use a higher percentage.

- 1% to 2% of Gross Profit (if gross profit is between $20,000 and $1,000,000): Companies with moderate gross profit would use a middle range percentage.

- 0.5% to 1% of Gross Profit (if gross profit is above $1,000,000 but less than $100,000,000): Larger companies with higher gross profits use lower percentages.

- 0.5% of Gross Profit (if gross profit is more than $100,000,000): Very large companies may use the smallest percentage.

By using these methods, auditors can set materiality thresholds that accurately reflect the company's financial realities. This ensures that financial statements are both reliable and meaningful to users.

What is the 5% Rule for Materiality?

Under US GAAP, the 5% rule suggests that if a misstatement is less than 5% of a financial statement item, it is generally considered not material. However this is not an absolute rule and must be applied with professional judgment. Some misstatements, though quantitatively small, may be qualitatively material due to their nature or context. Similarly, multiple small misstatements might collectively be material, even if each individual misstatement is not.

Connor Foran, former controller at Squarespace and Numeric’s Solution Lead adds this caveat as well:

“Generally, a company should have a lower materiality threshold than what their auditors and regulators require. You wouldn’t want to use 5% of net income and apply that to each general ledger account because if each was off by up to 5% of net income, that could be a really big number. So typically, accounting teams use a much lower threshold at the GL level and then potentially higher ones for the financial statement line item level.”

Challenges in Materiality Assessments

Applying materiality thresholds in practice comes with several challenges.

- Complex Transactions: Some industries deal with highly complex transactions that make it difficult to apply standard materiality thresholds.

- Judgment Variability: Different auditors may have varying judgments on what constitutes material information, leading to inconsistencies.

- Changing Regulations: Regulatory changes can impact materiality assessments, requiring auditors to stay updated and adapt quickly.

- Resource Constraints: Limited resources and tight deadlines can make it difficult to thoroughly evaluate materiality.

Best Practices in Materiality Assessments

To ensure consistent application of materiality thresholds, accounting teams can follow these best practices:

- Clear Guidelines: Establishing clear, detailed guidelines for materiality assessments help reduce judgment variability and improve consistency.

- Peer Reviews: Implementing peer reviews of suggested materiality thresholds can provide an additional layer of scrutiny and consistency.

- Use of Templates: Standardized templates for materiality calculations ensure uniformity across accounts.

- Regular Training: Continuous education and training the latest standards and practices helps maintain consistency.

FAQ About Materiality Assessments

How do you apply materiality thresholds in practice?

Applying materiality thresholds effectively involves a series of well-defined steps.

- Identify Key Financial Metrics: Determine which financial metrics are most relevant. Common metrics include revenue, net income, total assets, and equity. These metrics will serve as the basis for calculating materiality.

- Calculate Preliminary Materiality: Using the identified metrics, calculate preliminary materiality thresholds. For instance, you might set materiality at 5% of net income or 1% of total assets.

- Adjust for Qualitative Factors: Consider qualitative factors that might affect materiality, such as the nature of transactions, regulatory requirements, and potential for fraud. Adjust the preliminary thresholds accordingly.

- Document the Rationale: Clearly document the rationale behind the chosen materiality thresholds, including any adjustments made for qualitative factors. This documentation ensures transparency and consistency.

What materiality threshold should I implement ahead of my first-time audit?

Ahead of a first-time audit, teams should set materiality thresholds fairly low in order to have greater confidence in the accuracy of their financial statements. Because auditors will most likely not tell you the materiality they will be using to assess your documents, it benefits teams to implement a reasonably low threshold out of an abundance of caution.

How do materiality thresholds differ by industry?

Each industry faces unique risks that can influence materiality thresholds. For instance, the pharmaceutical industry might place a higher materiality threshold on research and development costs due to the high stakes involved in product development. On the other hand, a manufacturing company might focus more on inventory valuation. These industry-specific risks necessitate tailored materiality rules to ensure that the most critical information is highlighted in financial statements. Here are some other examples:

- Retail Industry: In retail, a materiality threshold might be set at 1% of total revenue due to the high volume of transactions and relatively low profit margins.

- Banking Sector: For banks, materiality might be calculated as 0.5% of total assets, given the large asset base and the critical nature of financial stability.

- Manufacturing: In manufacturing, 5% of net income might be an appropriate threshold, reflecting the importance of profitability and operational efficiency.

The Bottom Line

Materiality is just another way to think about what matters most – for accounting teams, investors, creditors, and whoever else might get a hold of financial statements. To stay atop of materiality thresholds, teams should identify industry-specific rules, any thresholds stated by their auditor, and continue to review existing thresholds to ensure they remain aligned with the most up-to-date guidance.

Related Content

.png)

.png)

Finance Process Improvement: A Comprehensive Guide For Mid-Market And Enterprise Teams

Finance process improvement is how you close the gap between what the business expects from finance and what your current workflows can actually deliver. This guide covers which processes to improve first, how to assess your current state, how to build a phased roadmap, and where technology fits in.

.png)

Finance Team Structure: How To Build A Modern Finance Organization

How to design a finance team structure that scales alongside your business — covering roles, reporting lines, structural models, centralization tradeoffs, and design principles for SaaS and high-growth companies.