Headed to the Big Leagues: The IPO Need-to-Know for Accountants

.webp)

The rumors have been swirling internally for months, but today, your CEO just made it official: the company plans to IPO in the near future.

You’re ecstatic — soon, the exec team will ring the bell in New York City and then, you’ll be public. That’s all it takes, right? A few chimes, a nifty company ticker, and then, the cash flows in.

We all wish it were that simple (okay, everyone except the SEC), but instead, the IPO process is tedious, complex, and lengthy. While the filing process may only take six or so months, readiness procedures can take the better half of two years.

Covering everything that happens in those two years would take us…well, about two years. Instead, we’ve assembled a streamlined guide for accountants on the key steps of the IPO process.

What is the IPO?

An IPO (Initial Public Offering) is the first public sale of a company's shares. Before an IPO, a company typically has a smaller group of investors—often founders, family, and private investors, like VCs. After an IPO, the company’s shares are available to the general public on a stock exchange. This initial sale allows the company to raise capital from a wider pool of investors, which can be used for expansion, paying off debts, or other financial needs.

The Pathways to Public: Traditional IPO, SPAC, & Direct Listing

Traditional IPO

A traditional IPO is the process through which a private company offers new shares to the public for the first time to raise capital. In this pathway, the company works with underwriters, typically investment banks, to help price the shares, market the offering, and manage regulatory compliance.

Advantages of Traditional IPOs

Access to Capital Markets: Traditional IPOs provide companies with a significant opportunity to raise new capital. The funds raised can be used for various growth initiatives, such as expanding operations, paying down debt, or investing in new technology.

Underwriter Support: The involvement of underwriters ensures that the IPO is marketed to a broad investor base. They help set an appropriate share price and can stabilize the market if volatility arises post-listing.

Challenges of Traditional IPOs

High Costs: The costs associated with traditional IPOs are substantial, including underwriting fees (often 7% of the total raised), legal expenses, and other advisory costs. This makes it one of the more expensive pathways to going public.

Lengthy Process: The traditional IPO process can be time-consuming, typically taking several months to over a year. It involves multiple regulatory filings, roadshows to pitch to investors, and SEC (Securities and Exchange Commission) review, which can delay a company’s plans to access capital.

Direct Listing

In a direct listing, a company offers its existing shares directly to the public without issuing new ones. This approach means the company does not raise new capital during the process. Instead, it allows current shareholders, such as employees and investors, to sell their shares on the public market.

Advantages of Direct Listing

No Underwriters: Unlike traditional IPOs, direct listings do not involve underwriters. This means the company bypasses the typical underwriting fees, potentially lowering transaction costs significantly. Companies save on costs associated with investment banks that usually manage and market an IPO.

Flexibility in Share Sales: Existing shareholders can sell their shares at any time once the company is listed. There is no lock-up period, which is common in traditional IPOs. This flexibility can benefit early investors looking to cash out.

Challenges of Direct Listing

Investor Base Control: Without underwriters, companies lose control over the initial distribution of shares. There is no guaranteed buyer base at the outset, which can lead to volatility in share price.

Trading Volume Concerns: The absence of underwriters means there is no initial price stabilization, which can create challenges in maintaining consistent trading volume. This lack of liquidity can deter potential investors.

SPAC

SPACs, or special purpose acquisition companies, are perhaps the most unique and nuanced of the IPO pathways. The Harvard Business Review defines them succinctly:

“A SPAC is a publicly traded corporation with a two-year life span formed with the sole purpose of effecting a merger, or “combination,” with a privately held business to enable it to go public.”

Following the de-SPAC merger, the previously private company now functions as a public corporation.

Advantages of SPACs

Faster Timelines: Since SPACs already have funds raised and are publicly traded, the process mainly involves negotiating and completing the merger. This efficiency allows companies to avoid the lengthy and complex procedures of a traditional IPO.

Capital Certainty: Companies engaging with a SPAC often know the amount of capital they will receive upon completion of the merger. This certainty can be particularly appealing for firms looking for predictable financial outcomes. The funds raised during the SPAC’s IPO are earmarked for the merger, ensuring available resources once a deal closes.

Challenges of SPACs

High Costs: While SPACs might expedite the process, they can incur significant costs that rival those of a traditional IPO. These include fees paid to the SPAC sponsors and other legal and advisory expenses.

Equity Dilution: SPAC sponsors typically receive a substantial equity stake in the merged entity, often around 20%. This can lead to dilution for existing shareholders, impacting their ownership percentages and potential returns.

Why Do Companies Go Public?

Companies choose to go public for several strategic reasons. An IPO can provide significant benefits that help a business grow and thrive in competitive markets.

Access to Capital

One of the main reasons companies go public is to raise funds by selling shares to the public. This influx of cash can be substantial. It provides the company with the resources needed for expansion—whether that means developing new products, entering new markets, or investing in infrastructure. Compared to private funding methods, public investors offer a much larger pool of potential capital.

Increased Visibility and Prestige

Going public often bolsters a company’s reputation. The process of an IPO brings attention from investors, analysts, and the media. This heightened visibility can enhance the company’s market presence, attracting new customers and partners. Being listed on a stock exchange is often seen as a mark of prestige, suggesting that the company has reached a level of maturity and stability.

Liquidity for Shareholders

An IPO provides liquidity, making it easier for shareholders to buy or sell shares. Before going public, selling shares in a private company can be challenging and often involves complex negotiations. Once public, shares can be traded on the stock market, offering shareholders more flexibility and easier access to cash. This liquidity can be attractive to early investors and employees with stock options.

Potential for Future Growth and Expansion

With the capital and visibility gained from an IPO, companies are well-positioned for future growth. Publicly traded companies often find it easier to acquire other businesses or form strategic partnerships. They can also use their public shares as currency in mergers and acquisitions. This potential for growth makes an IPO an appealing option for companies aiming to expand their influence and market share.

What is IPO Readiness?

IPO readiness refers to the process of gearing up a company to sell shares to the public for the first time, ensuring it can withstand the pressures and scrutiny of the public market. This preparation goes beyond just financial information; it involves fine-tuning operational processes and establishing a robust strategic plan. The stakes are high—failing to meet investor and regulatory expectations can damage a company's reputation and financial stability, making readiness essential for a smooth transition to public ownership.

To that end, most teams structure their IPO preparation with some of an IPO readiness assessment. An IPO readiness assessment acts as a diagnostic tool, pinpointing gaps in financials, corporate governance, and strategy before going public.

By identifying areas needing improvement early on, companies can address potential pitfalls and strengthen their market position. Think of it as a corporate check-up: catch the weaknesses now, and you'll save yourself from some serious public headaches later.

Why Financial Preparation is Crucial for IPO Readiness

As thousands of potential investors prepare to make some decision about the company and its future, it’s only natural that finances serve as the foundation for any conversation about a company’s public viability. In fact, to even register to go public, companies have to submit an S-1 registration statement with the SEC that gives an extensive history of the company’s finances.

If finance and accounting teams can be seen as a back-office function any other time, during the IPO readiness process, they’re the stars of the show. Preparing for an IPO requires a series of financial tasks that layer onto the existing work these teams already perform:

- Building internal controls: Obtaining SOX compliance is essentially at the top of the agenda for the accounting org. Doing so requires meticulous attention to current controls as well as educating one’s self about SOX requirements.

- Prepping financial statements: Companies are required to provide audited financials over the last 2-3 years as well as series of interim unaudited financial statements about current company performance.

- Working with external auditors: Where there’s accounting, there’s bound to be some auditors, no? During the IPO process, not only is external auditing quite rigorous, but finance teams are expected to build out an internal audit function as well

- Becoming public-ready: Most private company accounting doesn’t meet the expectations of the public realm. To get there, teams will have to revamp their close process, implement new technologies, revise processes, and likely hire new leadership and tons of help.

These tasks are just the tip of the iceberg: beyond them exists dozens, if not hundreds, of finance minutiae that teams must acknowledge and complete in advance of going public. That said, thorough financial preparation is not just a requirement; it is a strategic advantage. It empowers your company to enter public markets with confidence, ensuring long-term success and growth.

What are the Key Accounting Considerations for IPOs?

Navigating the accounting landscape of an IPO requires understanding several key components. Each plays a vital role in preparing your company for the scrutiny of public markets.

Understanding S-1 Financial Requirements and SEC Compliance:

- S-1 financial requirements: Filing an S-1 form with the SEC is one of the first steps in going public. This document contains detailed financial statements and disclosures about your company. It provides potential investors with critical insights into your business operations and financial health.

- SEC compliance: Ensures that your company meets all regulatory requirements. Non-compliance can result in delays or penalties, which could derail your IPO plans. It is crucial to work closely with legal and accounting experts to ensure that all filings meet SEC reporting standards.

Importance of Accurate Revenue Recognition and Addressing 'Cheap Stock':

- Accurate revenue recognition: This is essential for portraying a true picture of your financial performance. Misstating revenue can lead to serious legal issues and loss of investor trust. Adopting the correct accounting standards, such as ASC 606, helps in recognizing revenue accurately.

- 'Cheap stock' considerations: This term refers to stock options granted to employees at a price significantly below the IPO price. If not addressed, it can lead to large compensation expenses that must be recognized in your financial statements, affecting profitability.

Handling Acquisitions and Related Party Transactions:

- Acquisitions: When a company acquires another entity, it needs to consolidate the financials of the acquired company. This can be complex, especially if the acquisition occurs close to the IPO date. Proper valuation and integration of the acquired company's financials are crucial.

- Related party transactions: These involve dealings with entities or individuals related to your company. Such transactions must be disclosed in detail to avoid any perception of unfair advantage or conflict of interest. Proper documentation and transparency are key.

Significance of Internal Audits and Maintaining a Robust Control Environment:

- Internal audits: Internal audit teams serve as a check to ensure that internal controls are operating effectively. They help in identifying areas of risk and ensuring that financial reporting is accurate.

- Robust control environment: This involves establishing strong policies and procedures to ensure financial integrity. A well-maintained control environment reduces the risk of errors and fraud, reassuring investors of your company's stability and reliability.

These accounting considerations are not just technicalities; they are essential elements that influence the success of your IPO, ensuring that you present a financially sound and compliant company to the market.

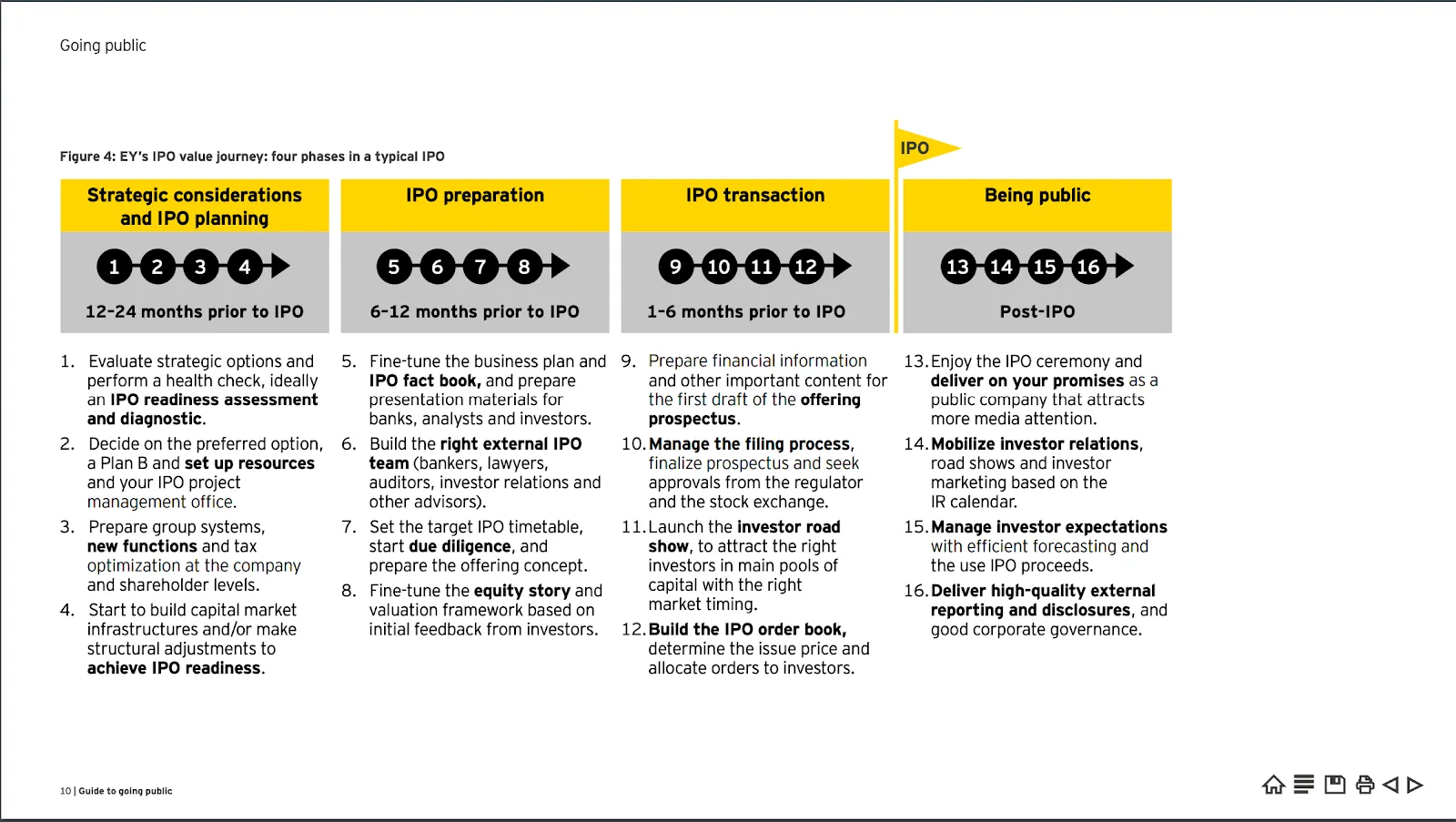

What is the IPO Timeline?

The IPO roadmap can be thought of in roughly four phases; planning, preparation, the IPO transaction, and then life as a public company.

Phase 1: IPO Planning

The planning phase establishes a solid foundation for a successful IPO by evaluating readiness and aligning with experienced advisors.

- Readiness Assessment: Examine financial health, governance structures, and operational maturity to ensure the company meets public market standards.

- Advisor Selection: Partner with investment banks, legal advisors, and auditors who specialize in IPOs to guide the company through each step.

- Strategic Positioning: Clearly define the company’s value proposition and market potential to attract investor interest and stand out in the market.

This groundwork prepares the company to meet the rigorous demands of going public.

Phase 2: IPO Preparation

In the preparation phase, the company tackles regulatory requirements, marketing efforts, and pricing strategies to make a strong market entry.

- Regulatory Filings: Complete and submit required documentation (e.g., SEC filings) to comply with regulatory standards and facilitate a smooth IPO.

- Investor Marketing (Roadshows): Engage potential investors through roadshows, where the company presents its business model, growth plans, and market appeal.

- Pricing and Allocation: Finalize the offering price based on investor demand and market conditions, ensuring an optimal balance between raising capital and retaining investor interest.

Thorough preparation ensures the company is positioned for a successful public launch.

Phase 3: IPO Transaction

In the transaction phase, the company transitions to the public markets and begins its relationship with new shareholders.

- Market Debut: Officially list on a stock exchange, marking the first day of public trading for shares.

- Investor Relations: Establish an investor relations strategy to maintain transparent communication and build investor trust.

- Compliance and Reporting: Implement ongoing financial reporting and regulatory compliance protocols to meet public company obligations and reporting requirements.

A well-executed transaction phase signals the company’s commitment to transparency and shareholder value from day one.

Phase 4: Post-IPO

After going public, companies focus on performance tracking, strategic growth, and proactive stakeholder communication to build credibility and sustain success in the market.

- Performance Tracking: Regularly monitor stock performance and market trends to inform strategic decisions.

- Beat-and-Raise Mindset: Cultivate a "beat-and-raise" approach by setting achievable targets and aiming to exceed them, which can foster investor confidence and stock momentum.

- Strategic Growth Initiatives: Pursue growth opportunities, including potential acquisitions, new product lines, or market expansions.

These phases provide a structured approach for companies considering going public, addressing both immediate actions and long-term strategies.

Put Your Team on the Road to IPO

Common Accounting Challenges for the IPO

Transition from Private to Public Accounting

Accounting under public scrutiny is no small feat. The largest change? Accounting orgs have to be compliant with SOX requirements, especially sections 404 and 302 which tend to require an overhaul of the internal controls process that can take up to a year to complete.

Without sufficient preparation, private accounting teams will struggle to adapt to the rigor of public accounting. This could lead the company to miss their initial set of earnings estimates, identify and subsequently disclose material weaknesses in their controls, and suffer reputational damage or fines at the hands of the SEC.

Cost & Dedicated Resources

Going public is expensive. In their 2023 Business Guide to IPOs, the Connor Group writes regarding IPO costs:

“High growth companies will pay millions of dollars in fees and costs to go public. Typical cost ranges can be from $3 to $5 million for an average IPO and $5 to $10+ million for a more complex organization (including legal, accounting, IPO readiness, investor relations, printers, etc.).”

While this challenge applies company-wide, accounting teams should be prepared to spend quite a bit in audit fees, accounting advisors, and hiring essential personnel.

Technology

Ever heard the adage “what got you here won’t get you there”? This sentiment applies wholly to the accounting tech stack and the IPO process. Without adequate investments in the right software, an uphill battle awaits in trying to scale the business.

As any accountant knows, software can make or break a team’s productivity. In addition, successfully integrating a tool can take over a year from start-to-finish. Failure to properly evaluate and administer technologies can delay other IPO readiness tasks and ultimately, the IPO altogether.

Time Management

Just like the crunch that comes during audit season, IPO preparation brings on the expectation that accountants complete both their standard accounting tasks as well as the tasks related to going public. Between normal closing, process review, auditor conversations, and compiling the S-1, there’s no shortage of important tasks to go around. As such, the management team will have to be highly intentional about which tasks are best fit for their current accounting team and which might call for external help.

Personnel

If accounting teams already feel stretched for human resources, then getting ready to go public is an even more brutal test of team output. It’s nigh impossible for companies to achieve an IPO without scaling their accounting team.

That said, the accountant shortage hasn’t made the hiring process any easier and finding people with technical accounting proficiency and IPO readiness experience can take great time and/or money. It’s also possible that companies without a CAO will need to hire one to help put the accounting team on the right path to public accounting compliance.

Best Practices for IPO Readiness in Accounting

Start Early

What do Big 4 Firms have to say about IPO readiness?

EY: “Successful IPO candidates often spend two years or more building business processes and infrastructure, recruiting executive and advisory talent, getting in front of financial and reporting issues and mastering the essential board of directors’ commitment to go public.”

KPMG: “A key success factor for getting a pre-IPO company through Sarbanes-Oxley (SOX) compliance is starting early. While timing may vary by company size, structure, number of locations, in scope, etc., it takes at least a year or more to get a company though its initial SOX compliance effort.”

PwC: “The most successful companies operate as if they were public companies prior to going public.”

It’s clear: to set your company up for success, accounting & finance organizations need to be preparing for public operations at least two years from public debut. Early action allows time to implement accounting policies, update systems, and address gaps identified across the organization.

Ramp Up Controls & Internal Audit Operations

When speaking on her company’s path to IPO, Interim CFO Lindsay Gray mentioned that it took her team roughly a year to run a strong SOX operation. She recommends that management express the importance of SOX controls and train employees to understand the value of spending time on controls-related work in addition to day-to-day tasks.

Equally important? Gray says that it’s essential to get the company’s internal audit group dialed up before or soon after an IPO. In doing so, teams can better identify risks, improve the efficiency of their operations, and most importantly, stay compliant. The success of an IPO often hinges on a company’s internal audit and its ability to create a robust control environment. Teams must evaluate their systems for GAAP alignment and ensure compliance with PCAOB auditing standard

Re-Evaluate and Revamp Tech Systems

In their 2023 Material Weakness Study, KPMG states,

“Companies should not overlook the technology aspect of financial reporting. Often systems used by private companies are not able to scale to the requirements of public companies.:

In preparing for an IPO, teams should ask themselves these types of questions:

- Is my ERP supportive enough for the growth my company expects?

- Is there cohesion between my existing software?

- Do I need dedicated audit software ahead of the IPO?

- Will my IT teams be able to help in the implementation and onboarding of new tools?

- Can I implement AI tools or automation to expedite current workflows?

Building out a tech stack that can support company initiatives is valuable at any time, but especially during the company’s public readiness phase.

Dedicate Resources

It’s common for teams to generally underestimate the amount of resources needed throughout the IPO process, but accounting teams really require more help and attention than ever before. In addition to learning on outside, advisory service consultants for assistance, hiring will need to increase. To handle these changes, it helps to designate specific employees to lead the project management effort for tasks across the IPO readiness docket.

The Bottom Line

An IPO is a defining moment for any company, but success hinges on preparation. From refining financials to strengthening processes, the work done before going public shapes both the IPO and the company’s future. By starting early, addressing gaps, and staying focused on long-term goals, companies can navigate the challenges of going public and position themselves for continued sustainability and market credibility.

Related Content

.png)

.png)

Finance Process Improvement: A Comprehensive Guide For Mid-Market And Enterprise Teams

Finance process improvement is how you close the gap between what the business expects from finance and what your current workflows can actually deliver. This guide covers which processes to improve first, how to assess your current state, how to build a phased roadmap, and where technology fits in.

.png)

Finance Team Structure: How To Build A Modern Finance Organization

How to design a finance team structure that scales alongside your business — covering roles, reporting lines, structural models, centralization tradeoffs, and design principles for SaaS and high-growth companies.