Segregation of Duties Explained

.webp)

When financial processes lack oversight, the consequences are costly—fraud, misstatements, and audit findings, to name a few.

Segregation of duties in accounting is the first line of defense, designed to prevent such risks by dividing tasks among multiple team members. It's not just about compliance; it's about creating a framework where accountability thrives and errors are caught before they escalate.

This article dives into the essential components of segregation of duties, practical examples for accounting teams, and solutions for overcoming challenges in implementation.

Understanding the Importance of Segregation of Duties in Accounting

Errors and fraud are constant challenges in accounting. When one person has too much control over financial processes, the organization faces serious risks.

Segregation of duties (SOD) is a key internal control designed to reduce those risks by dividing responsibilities across multiple individuals.

For teams working with complex accounting systems, SOD is a necessity. Whether handling account reconciliations, managing approvals, or recording transactions, splitting responsibilities promotes accountability and protects financial integrity. Dividing these tasks not only shields the organization from risks but also helps streamline processes for better efficiency.

Defining Segregation of Duties (SOD)

Segregation of duties involves splitting essential accounting tasks among various individuals to reduce errors and prevent fraud. It ensures that no one person has unchecked authority over critical financial processes. Separating roles like transaction authorization, recordkeeping, and asset management creates a reliable system of checks and balances.

The goal is to prevent conflicts of interest and limit opportunities for fraud. For example, the same individual approving payments should not also reconcile bank accounts. This separation strengthens accountability and enhances internal controls.

Core Components of SOD

Effective implementation of SOD requires focusing on four main areas:

- Authorization: Approving transactions is the first control layer. Only specific individuals should have the authority to approve expenditures, journal entries, or vendor payments.

- Recording: Proper documentation and accounting entries are essential. Assign recording duties to individuals who are separate from those approving or reviewing the transactions.

- Custody of Assets: Control over resources like cash, inventory, or financial systems must be limited to designated roles. Those managing assets should not also have the ability to authorize or record transactions.

- Reconciliation: Comparing records to ensure accuracy is the final step. Reconciliation tasks should be performed by someone independent of those approving or recording transactions to maintain objectivity.

Development of SOD Matrices and Governance Frameworks

SOD matrices serve as visual tools to identify conflicting responsibilities and pinpoint risks. By mapping out how tasks are assigned, accounting leaders can identify areas where adjustments are needed.

Governance frameworks provide additional protection by defining protocols to detect and address conflicts. For instance, periodic audits or other compensating controls can help mitigate risks in situations where small teams make full segregation difficult.

Role-based access controls play a vital role in maintaining segregation within digital systems. Permissions should align with SOD principles to block unauthorized access or data manipulation. A reliable system administrator is essential for managing these controls, ensuring financial systems remain secure and compliant with accounting standards.

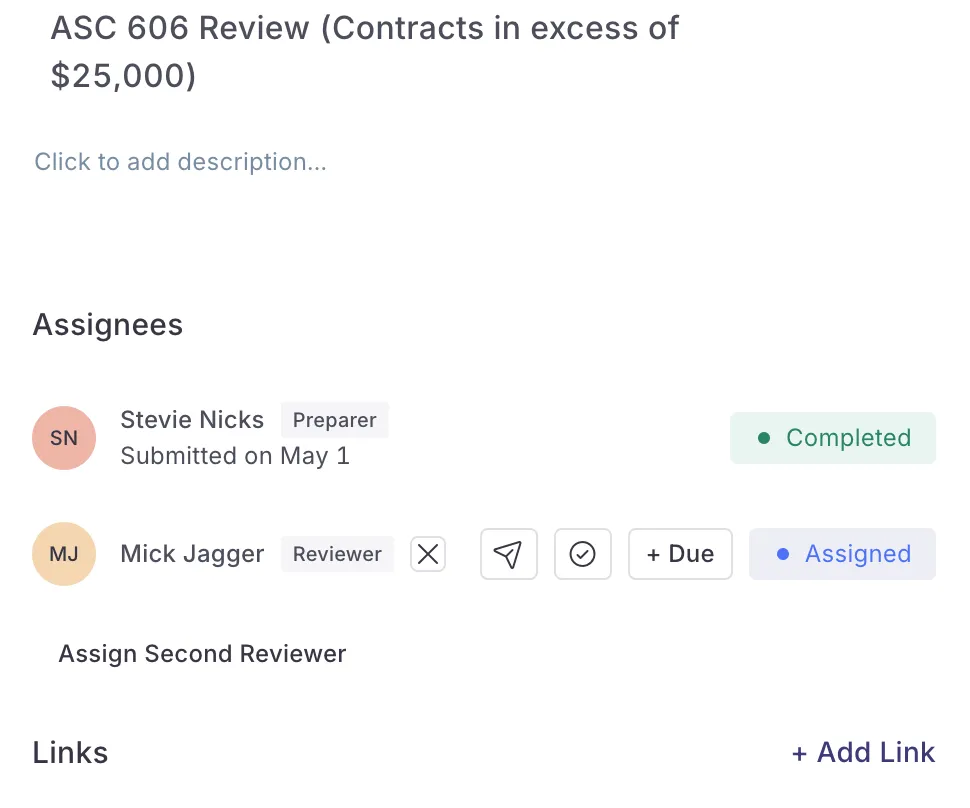

Numeric gives administrators the chance to assign roles with different permissions to users in the workspace. For example, accountants can invite their auditors to view, but not edit their reconciliations, review comments, and overall financial data. Multientity organizations can prevent accounting teams from one entity from accessing the data of another. Implementing segregation of duties in accounting is crucial for maintaining accurate financial records, reducing risks, and ensuring compliance with regulations — and Numeric makes it easy to implement these controls.

The Critical Role of Segregation of Duties in Internal Controls

Enhancing Risk Management

Segregation of duties (SOD) helps protect against fraud by ensuring no one person has full control over critical financial tasks. Dividing responsibilities across different roles creates checkpoints that make it much harder for fraudulent activities to go unnoticed.

In Numeric, accounting teams can organize their month-end, quarter-end, and year-end close tasks and subsequently are able to assign a preparer and a reviewer to each task. When tasks such as transaction approvals, recordkeeping, and reconciliations are assigned to separate individuals, mistakes are more likely to be spotted early. This reduces the chances of those errors escalating into bigger problems.

Regulatory Compliance and Standards

Many laws and regulations require SOD as a fundamental part of internal controls. For instance, the Sarbanes-Oxley Act (SOX) mandates public companies to establish and maintain controls like SOD to ensure their financial reporting is accurate.

Auditors often assess the effectiveness of SOD when evaluating financial reporting. Without a clear separation of roles, auditors frequently flag material weaknesses, which can delay filings or lead to penalties. Roles such as '404 Control Specialists' are often tasked with overseeing compliance with SOX Section 404, making sure SOD frameworks remain strong and effective.

Strengthening Organizational Integrity

Effective segregation of duties boosts trust among stakeholders by reinforcing the reliability of financial processes. Investors, regulators, and employees tend to have greater confidence in companies that take steps to prevent fraud and errors. Strong financial systems lead to better, more informed decisions.

Within the organization, SOD creates accountability by clearly defining responsibilities. Employees are less likely to stray from established procedures when oversight is in place. This transparency helps create a culture of reliability, reducing risks and strengthening the organization's control systems.

Internal Controls as a Competitive Advantage

Strong internal controls, including SOD, do more than meet regulatory obligations—they can add significant value to a business. By creating smoother processes and lowering the chances of costly mistakes or fraud, companies present themselves as reliable and well-managed.

Companies with dependable controls often stand out during audits, acquisitions, or public offerings, as transparency makes them more appealing to stakeholders. A well-executed SOD framework also supports operational efficiency, allowing accounting teams to focus on strategic projects instead of constantly addressing preventable issues.

Reliable financial reporting relies on trustworthy data.

Reduce audit headaches with a clear audit trail

.png)

Practical Examples of Segregation of Duties in Accounting Processes

Here are straightforward examples of how accounting teams can put the practice of separating responsibilities in accounting processes into action.

Accounts Payable and Receivable

- Invoice Approval vs. Payment Processing: Have one person approve invoices and another handle payment processing. This separation makes sure the person approving a payment is not the one executing it.

- Billing and Collections: The team responsible for sending invoices should not manage collections. This minimizes the chance of unauthorized changes to customer accounts or mishandling of payments.

Cash Handling and Banking Activities

- Cash Receipts vs. Bank Reconciliation: Employees who receive and record cash should not be responsible for reconciling bank statements. This step helps avoid tampering with deposits or hiding inconsistencies.

- Deposit Preparation vs. Cash Entry Recording: The task of preparing bank deposits should go to someone different from the person recording the deposit entries. Assigning these roles separately ensures accurate cash tracking and prevents possible manipulation.

Payroll Management

- Onboarding, Timekeeping, and Payroll Disbursement: HR can oversee employee onboarding, department managers can track timekeeping, and the accounting team can manage payroll disbursements. Splitting these responsibilities helps prevent unauthorized or fraudulent payroll activity.

- Preventing Ghost Employees: The person processing payroll should not have access to add new employees to the system. This safeguards against payments being made to non-existent employees.

Inventory and Asset Management

- Ordering, Receiving, and Recording: Ensure that the person placing orders for inventory isn't also managing receipts or recording transactions. This process reduces the risk of tampering with stock levels or misusing goods.

- Physical Inventory Counts and Recordkeeping: Have someone who does not handle recordkeeping perform physical inventory counts. This independent verification increases accuracy and deters fraud.

Supporting SOD Across Reconciliations with Numeric

Segregation of duties requires deliberate processes, clear task ownership, and reliable tools to ensure everything works as intended. Numeric's reconciliation product integrates seamlessly with SOD principles, helping accounting teams implement and maintain this key internal control efficiently and accurately.

- Role-Based Access: Permissions determine who can view, edit, and approve reconciliations, ensuring the process aligns with SOD principles. This prevents one person from both preparing and approving a reconciliation, lowering the likelihood of errors or fraud.

- Automated Alerts: Notifications highlight discrepancies or overdue reconciliations, drawing attention to risks before they grow. This system keeps tasks monitored and ensures issues are addressed by the right individuals.

By automating parts of the reconciliation process, this tool reduces manual work while maintaining SOD, even as teams expand or processes become more intricate.

Overcoming Challenges in Implementing Segregation of Duties

Constraints in Small and Medium-Sized Enterprises

Small and medium-sized enterprises often face challenges with limited staff, making segregation of duties harder to implement. When resources are stretched thin, finding practical ways to maintain internal controls becomes even more important.

Limited Staffing:

- Train employees to handle multiple roles and rotate duties regularly to prevent over-reliance on one person.

- Increase management oversight to serve as a compensating control. Managers can actively review and approve critical activities to address gaps caused by limited segregation.

Over-Reliance on Key Employees:

- Depending too much on a few employees with deep institutional knowledge can create risks, especially if processes are not thoroughly documented.

- As the organization grows, it becomes necessary to formalize processes and establish standard operating procedures to ensure continuity and scalability.

Balancing Efficiency with Control Measures

A frequent concern with segregation of duties is the perception that dividing responsibilities slows operations. This worry is especially common in high-growth businesses or industries where speed is critical.

- Address these concerns by using technology to streamline processes. Automated systems can enforce role-based access controls, ensuring compliance without creating slowdowns.

Risk-Based Focus to Improve Efficiency:

- Concentrate on high-risk areas, such as transactions involving large sums or critical accounts. By focusing resources on these areas, businesses can reduce review costs and improve efficiency.

- Identify tasks where automation or alternative controls can reduce manual reviews and balance compliance with operational needs.

Cost Considerations

Budget constraints can make businesses hesitant to invest in segregation of duties. While the upfront costs may seem high, the long-term benefits far outweigh the risks of fraud or financial errors.

- Preventing fraud or costly mistakes requires proactive action. Even one instance of fraud can lead to financial losses, reputational harm, and increased scrutiny from auditors.

- Weigh the cost of implementing segregation against the risks it mitigates. Focus on measures that align with your risk tolerance and business priorities to make the best use of resources.

Employee Perceptions of Internal Control Initiatives

Internal control efforts, including segregation of duties, can sometimes be met with resistance from employees who see them as overly bureaucratic or unnecessary. Shifting this mindset requires clear communication and alignment with the company's values.

- Help employees understand the importance of strong internal controls by explaining how segregation reduces risks for both the company and its staff.

- Present controls as tools for improving operations rather than compliance burdens. Emphasize their role in boosting efficiency, transparency, and accuracy.

- Build a culture that values compliance and accountability. Promote ethical behavior through ongoing training and consistent enforcement of policies to reinforce the importance of internal controls.

Best Practices for Implementing Segregation of Duties

Conduct a Risk Assessment

Start by identifying where risks are most likely to occur within accounting processes. Focus on areas like cash handling, payroll, and financial reporting, where errors or fraud could have serious consequences. Map out how responsibilities are currently assigned to pinpoint overlaps or gaps that could create conflicts.

After identifying high-risk areas, address situations where one person controls multiple critical tasks. For instance, if one individual approves invoices and also reconciles bank accounts, reassign one responsibility to another team member. A well-documented assessment provides the groundwork for effective internal controls.

Create Clear Policies and Procedures

Define and document specific roles and responsibilities for all accounting processes. Clearly outline who approves transactions, who records them, and who reconciles accounts. Avoid leaving room for confusion by establishing detailed protocols for authorization, review, and escalation.

Review and update policies regularly to reflect changes in business operations or regulatory requirements. For example, if the company expands into a new region, adjust procedures to address risks specific to that market. Well-documented policies ensure consistency and serve as a useful reference during training or audits.

Here’s what Ben Sheridan, Numeric Solutions + Product Manager & former Big 4 accountant, had to add about segregation of duties policies:

“Segregation of duties is straightforward for manual journal entries: the approver must differ from the preparer, typically someone at a higher level (e.g., an accounting manager reviewing the work of a senior accountant).

This principle also applies to accounting-adjacent business processes. For instance, limits should exist on who can sign an order form with a customer—separating this role from the salesperson closing the deal. Similarly, for expense or procurement approvals, ensure the reviewer is distinct from the submitter. Additional layers of review may include checks for budget limits, accounting application, or vendor verification (e.g., confirming the vendor is on an approved list and not from a sanctioned country).”

For a full breakdown of how journal entry controls fit into the broader GL posting workflow, see our step-by-step GL posting guide.

Use Technology and Automation

Adopt software solutions to enforce segregation of duties in a systematic way. Role-based access controls help ensure users can only perform actions within their assigned responsibilities. For example, systems can restrict access to prevent someone from both approving and processing a transaction.

Numeric’s close checklist supports SOD by helping accounting teams to organize processes and ensure accountability during the month-end close.

- Context for Each Task: This feature delivers detailed documentation and step-by-step instructions for every task involved in the close process. By defining ownership clearly, it avoids overlapping responsibilities and strengthens the separation of duties for critical financial activities.

- Clear Accountability: Tasks are assigned to specific team members, reducing confusion and ensuring no single person has unchecked control over important activities.

This tool acts as a guide for accounting teams, embedding SOD principles into workflows for responsibilities like approvals and reconciliations.

Train and Raise Awareness

Educate employees on why segregation of duties is important and how it protects the organization. Offer training sessions that explain risks and show employees their role in maintaining controls. Use examples or case studies to highlight potential consequences of poor segregation.

Promote a culture of accountability and ethical behavior. Employees are more likely to follow procedures when they understand their value and feel involved in the process. Regular training refreshes help keep everyone aligned with control practices.

The Role of Segregation of Duties in IT Systems and Cybersecurity

As accounting processes increasingly rely on IT systems, digital transformation brings new risks to the table. Segregation of duties helps reduce these risks by ensuring no single person has unchecked authority over sensitive operations. In IT environments, this concept goes beyond traditional accounting roles, covering system access, cybersecurity, and data security.

Importance in Digital Accounting Systems

Modern accounting systems manage large amounts of sensitive financial data. Separating duties within IT frameworks strengthens security and reduces exposure to risks.

- Assigning appropriate user access levels: Match access rights to job responsibilities to prevent unauthorized entry into financial systems, such as general ledger entries or approval processes.

- Safeguarding financial data: Limit access to critical systems, allowing only those with a legitimate business need to make changes to data or system configurations.

Implementing IT Controls

IT controls grounded in segregation of duties help maintain secure operations and ensure financial teams can rely on the systems they use for reporting and analysis.

- Role-Based User Access Management: Design permissions around job functions using role-based access controls. For example, team members reconciling accounts should not also have the ability to approve journal entries, keeping critical tasks distinct and secure.

- System Audits and Activity Monitoring: Regularly review audit logs to catch unauthorized access or suspicious activity. Any irregularities, such as attempts to override permissions, should prompt immediate investigation to prevent breaches.

Preventing Cybersecurity Threats

Separating duties within IT teams strengthens safeguards against both external hackers and insider threats. Clear boundaries make it harder for financial systems to be manipulated or compromised.

- Dividing responsibilities between IT roles (e.g., developers vs. system administrators): Developers should not deploy code directly into production environments, and system administrators should not alter application code. This separation reduces the risk of system vulnerabilities caused by intentional changes or accidental errors.

- Minimizing internal breaches or data manipulation: Use multi-factor authentication and conduct regular access reviews to restrict critical system access. Restricting any one IT employee's ability to bypass controls protects financial systems from being compromised.

Consequences of Inadequate Segregation of Duties

Increased Risk of Fraud and Financial Misstatement

When responsibilities aren't divided properly, the chances of fraud increase significantly. For example, in one multinational organization, a single employee had control over both vendor setup and payment approvals. Over time, they redirected millions into fake accounts, remaining undetected for years due to unchecked authority. Without proper segregation, fraudulent actions like this can remain hidden until the financial damage becomes overwhelming.

Mistakes also thrive when duties aren't divided. If one person is tasked with both recording transactions and reconciling accounts, they might miss discrepancies. Over time, these errors can build up, leading to major inaccuracies in financial reports and compromising the reliability of the company's financial records.

Regulatory Penalties and Legal Implications

Regulations like SOX require companies to implement strong internal controls, and failing to meet those standards can result in hefty fines. Regulatory bodies often impose penalties in the millions for companies that lack adequate segregation of duties. For instance, businesses flagged for weak controls frequently deal with delayed filings and increased scrutiny during audits, which adds to compliance expenses.

The damage isn't just financial—it also affects reputation. Stakeholders may lose faith in companies with flawed internal controls, causing a decline in investor trust and, in severe cases, a drop in market value. Publicized control issues can strain relationships with regulators, auditors, and shareholders, creating long-term difficulties in regaining credibility.

Operational Inefficiencies

Fraud investigations or error corrections caused by poor segregation often disrupt normal operations. Teams are pulled away from their core responsibilities to address control failures, slowing down critical processes like financial closing and delaying reporting functions. For accounting teams already managing complex tasks, these interruptions can significantly reduce productivity.

On top of that, fixing the problem comes with its own costs. Businesses need to dedicate time and resources to establish new controls, train employees, and redesign workflows. Although these steps are necessary, they divert attention and funding from other strategic priorities, making it harder for the organization to function smoothly.

Sustaining Effective Segregation of Duties

Maintaining segregation of duties is an ongoing process that extends beyond setting up initial controls. Accounting teams need to continually adjust frameworks to align with shifting business demands while strengthening internal controls. Without consistent effort, even the strongest systems can weaken, leaving organizations vulnerable to mistakes or fraud.

Periodic Review and Adjustment of Controls

- Adapting to organizational changes: Companies often grow, restructure, or shift strategies, leading to changes in roles and responsibilities. During transitions like mergers, acquisitions, or departmental growth, teams need to evaluate segregation frameworks to ensure workflows still follow proper task separation.

- Improving control activities over time: Regularly review how effective the controls are. Gather feedback from employees, address new risks, and consider updates in technology to fine-tune processes and keep controls both effective and relevant.

Internal Audits and External Assessments

- Regular audits to check effectiveness: Plan periodic internal audits to confirm segregation policies are being followed. Pay close attention to high-risk areas like cash handling, vendor management, and payroll disbursements. Identifying and addressing any gaps quickly can help prevent future issues.

- External reviews for unbiased insights: Third-party experts can provide an objective look at the controls in place. They often uncover risks or inefficiencies that might be overlooked internally and can offer practical recommendations to address them.

Building a Culture of Accountability

- Management's role in enforcing policies: Leaders need to lead by example, following segregation policies themselves and ensuring their teams do the same. When leadership is visibly committed, it sends a clear message that these controls are a priority.

- Fostering responsibility and ethical behavior among employees: Create an environment where employees feel a sense of responsibility for maintaining internal controls. Offer ethics training and encourage staff to report irregularities or share suggestions for improvement without fear of consequences.

Bottom Line

For accounting teams managing growing complexity, segregation of duties is non-negotiable. It protects your organization from risks, instills confidence in stakeholders, and ensures compliance with critical regulations like SOX. By implementing strong controls and leveraging tools that support task separation, you can foster accountability and position your team for long-term success—even in the face of evolving challenges.

Related Content

Numeric Hosts The First Finance Engineer Cup

Four accountants built real AI tools for their own close and competed live. See how Alexandria Ramirez won Numeric's first Finance Engineer Cup.

The Finance Engineer: Why Accountants Are the Best Builders in the Room

Why accountants, not engineers, are becoming the best builders on modern finance teams. Meet the Finance Engineer.

.png)

Numeric vs. Ledge: What's the Best Close Platform for Your Business?

A detailed comparison of Numeric and Ledge, two modern close management platforms, covering features, architecture, pricing, and a framework for choosing the right fit for your team.